Banks and Credit Unions: The Digital Experience Landscape

Revealing where financial institutions are succeeding, where they're struggling, and what they're prioritizing next.

Executive Summary

The results from our survey illustrate a financial services market that is not debating whether digital experience matters. Banks and credit unions largely agree that CX, data, personalization, and AI will define the next phase of competition. The gap is not intent; it is execution.

Banks are more likely to describe their biggest constraint as disconnected data and internal inefficiency. Credit unions are more likely to surface personalization, journey complexity, and member engagement as the harder problems to solve. Both groups are operating in the middle: digital experiences are often strong enough to function but not differentiated enough to win.

The mandate is clear: move from channel-by-channel improvement to connected experience orchestration. Institutions that can unify data, simplify journeys, improve marketing speed, and apply AI responsibly will be better positioned to defend relationships and create new growth.

Focused Market Context

Three market forces provide important context for the survey findings:

- AI Adoption: Financial institutions continue increasing investment in AI, but many organizations remain in pilot mode rather than scaled production deployment. This mirrors the survey finding that both banks and credit unions are still navigating the gap between experimentation and operationalization. [4] [5] [6]

- Rising Customer Expectations: Consumers increasingly expect relevant, personalized, and seamless digital experiences. Yet survey respondents reported low confidence in their ability to consistently deliver personalization across channels. [17] [18]

- Technology Complexity: Martech and customer experience ecosystems continue to grow more complex. Survey respondents repeatedly identified disconnected data, siloed systems, and execution friction as barriers to delivering better experiences. [11] [20] [21]

Against this backdrop, the survey results reveal where banks and credit unions are making progress and where execution challenges continue to slow transformation.

External market context

- The FDIC reported that 48.3% of banked U.S. households used mobile banking as their primary account-access method in 2023, nearly nine times the rate a decade earlier. [1]

- ABA/Morning Consult reported in 2024 that 55% of bank customers used mobile apps most often to manage their accounts, while another 22% used online banking via laptop or PC. [2]

- Deloitte’s 2026 banking outlook notes that AI programs are often constrained by fragmented data foundations, compliance demands, legacy systems, and isolated proofs of concept. [3]

Core Insight: The Experience Gap Is Now an Operating Model Gap

The strongest theme across responses is that banks and credit unions are not short on priorities. They are short on connected execution capacity. The same barriers appear repeatedly: fragmented systems, limited personalization, inconsistent omnichannel delivery, and slow campaign execution.

For digital marketing leaders, this shifts the conversation from “what should we improve?” to “what must be connected so improvement can scale?” That distinction matters. A better homepage, campaign, or account-opening flow may deliver short-term gains, but durable differentiation depends on the shared data, content, decisioning, governance, and measurement layer underneath.

The challenges identified throughout this report closely mirror broader industry trends around digital expectations, AI adoption, data integration, and personalization maturity. [3][11][17][20]

Survey Findings

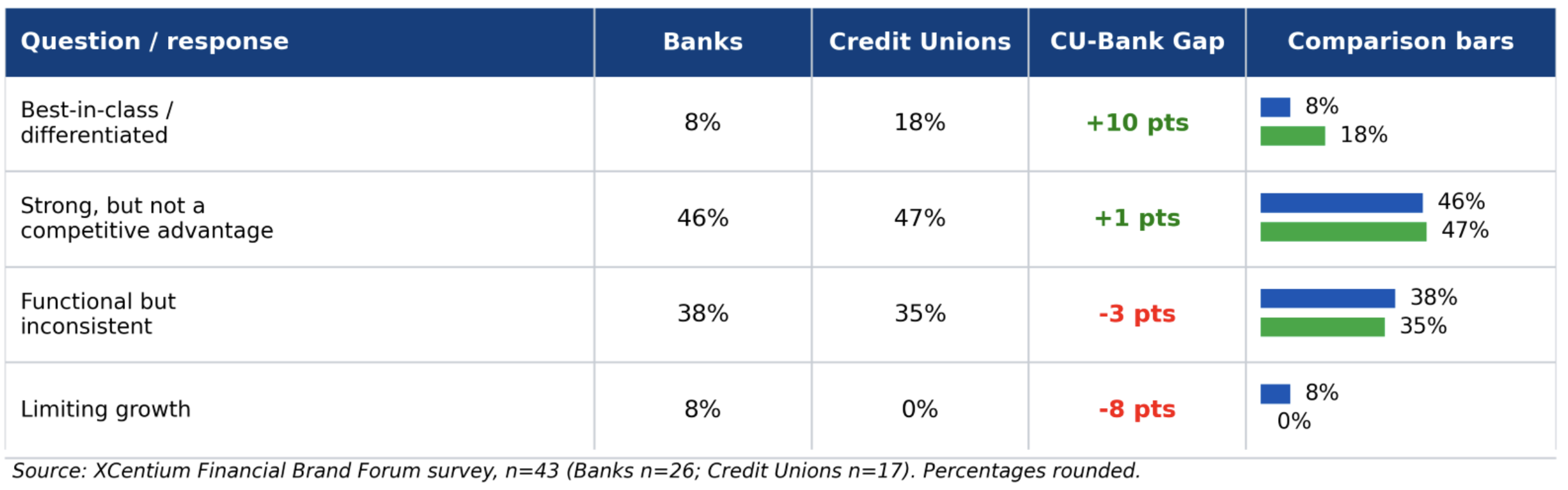

1. Digital CX Maturity: Most Institutions Have Achieved Competence, Not Differentiation

Banks 46% and Credit Unions 47% describe their CX as strong but not a competitive advantage. Only 8% of banks and 18% of credit unions describe experiences as differentiated.

Insight: Banks and credit unions cluster around the same uncomfortable middle: strong enough to operate, but not strong enough to differentiate. Credit unions show a slightly higher share calling their experience best-in-class, while banks show more respondents saying CX is directly limiting growth. The shared risk is complacency: “strong but not a competitive advantage” is not a defensible position when digital-first expectations continue rising.

Executive Implication: Incremental UX improvements will not create durable advantage. Institutions must connect data, content, and journey orchestration. Execution maturity is becoming the new competitive advantage.

Why this matters ...

- Most institutions now offer competent digital experiences, making differentiation (not functionality) the new competitive battleground. [8][9]

- Consumers increasingly compare banking experiences against digital leaders in other industries, raising expectations for simplicity, speed, and personalization. [10]

- Institutions that remain in the “strong but not differentiated” category risk losing growth opportunities to competitors that reduce friction across acquisition, servicing, and relationship expansion. [9] [10]

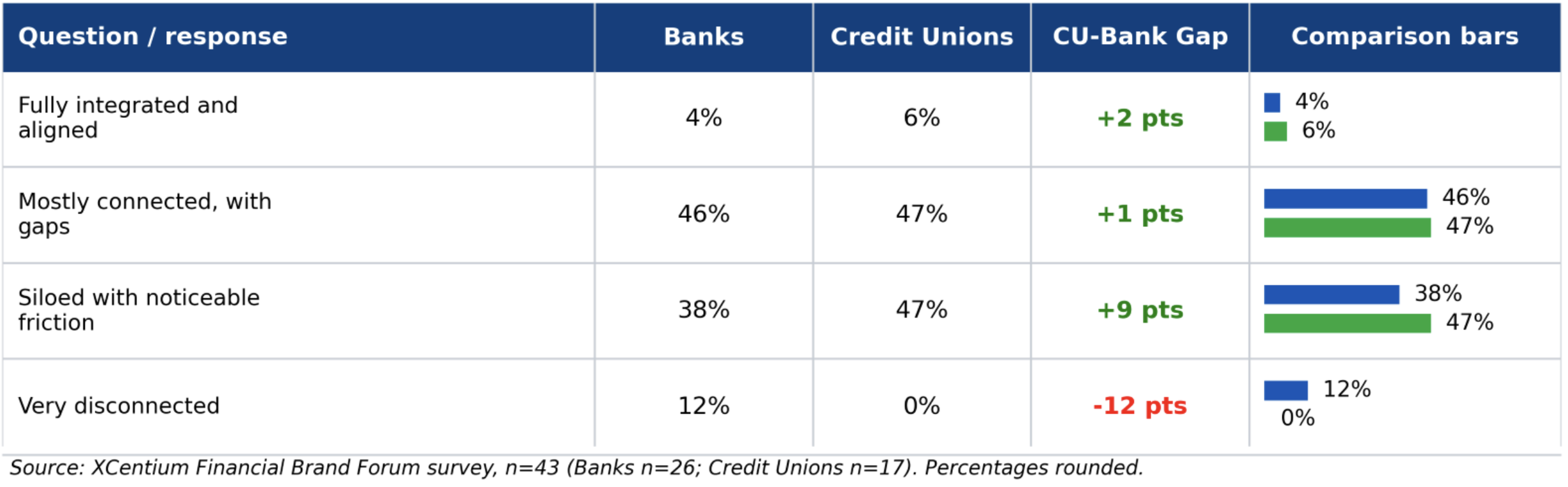

2. System Integration: Connected Enough to Function, Not Enough to Orchestrate

Only 4% of banks and 6% of credit unions report fully integrated ecosystems.

Insight: Both audiences report a similar level of partial connection, but the friction profile differs. Nearly half of credit unions describe systems as siloed with noticeable friction, while banks are more likely to report very disconnected environments. This suggests banks may face a deeper data architecture issue, while credit unions may feel the day-to-day operating pain of systems that technically connect but do not support smooth execution.

Executive Implication: Integration is no longer an IT initiative. It is a growth initiative. Execution maturity is becoming the new competitive advantage.

Why this matters ...

- AI, personalization, analytics, and journey orchestration all depend on connected customer data and integrated systems. [11] [13]

- As technology stacks expand, institutions with disconnected platforms face higher operating costs, slower execution, and limited visibility into customer behavior. [11][12]

- Organizations that modernize integrations and data flows will be better positioned to launch new experiences faster and adapt to changing customer expectations. [12] [13]

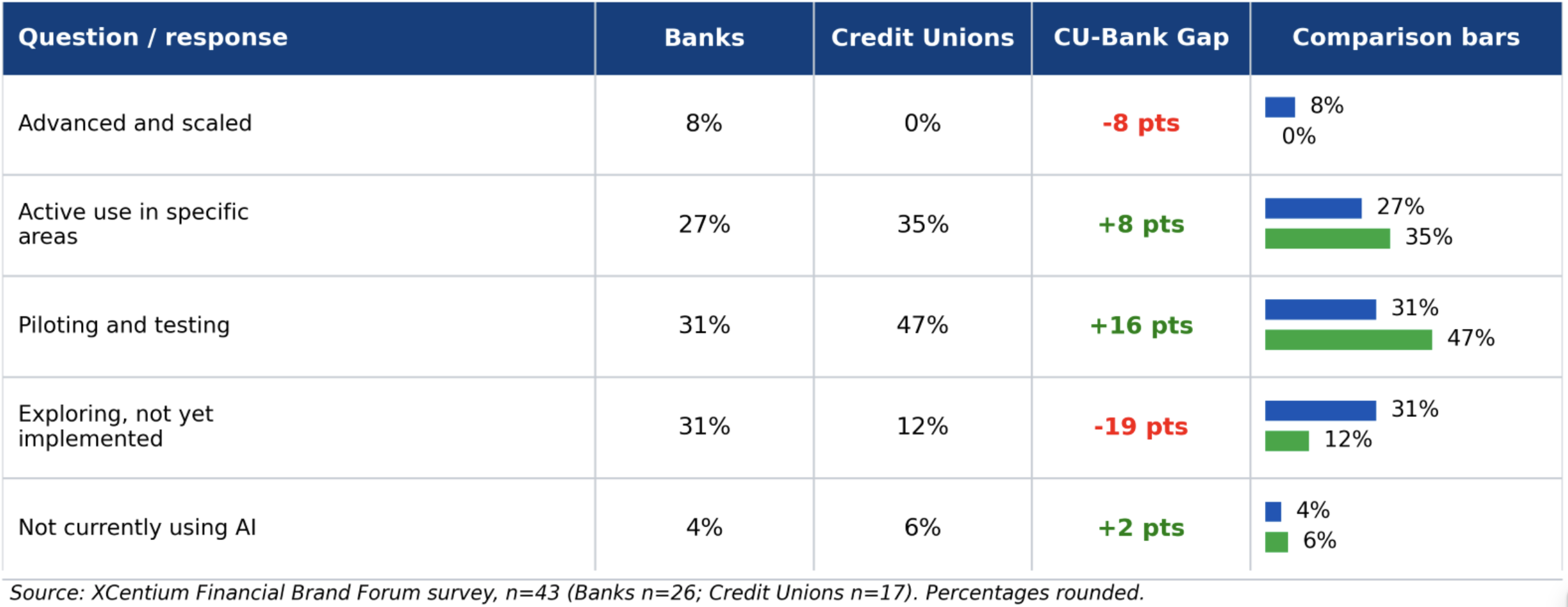

3. AI Readiness: AI Has Moved Beyond Exploration

Most respondents are actively using AI or piloting initiatives. Credit unions skew toward experimentation while banks show wider maturity variance.

Insight: Credit unions in this sample are more concentrated in pilot and active-use stages, while banks are split across exploration, piloting, and active use. The finding does not imply that credit unions are more mature overall; rather, it suggests credit unions may be moving quickly into practical experimentation. Banks show more scaled AI responses, but also a larger exploration cohort, pointing to uneven maturity inside the bank segment.

Executive Implication: The next challenge is operationalization, governance, and measurable value. Execution maturity is becoming the new competitive advantage.

Why this matters ...

- Financial institutions are rapidly moving from AI experimentation toward practical use cases focused on service, efficiency, risk management, and marketing performance. [14][15][16]

- The competitive advantage is shifting from simply adopting AI to governing, operationalizing, and scaling it effectively. [14]

- Institutions that connect AI initiatives to measurable business outcomes will realize greater value than those treating AI as a standalone technology project. [14][15]

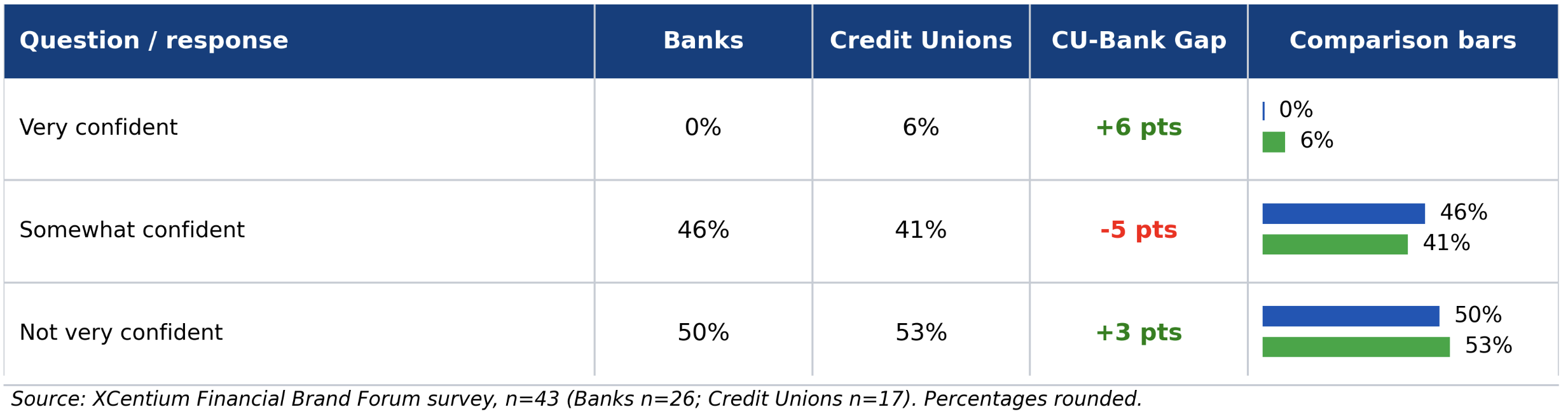

4. Personalization Confidence: The Shared Confidence Gap

Approximately half of respondents lack confidence in personalization capabilities.

Insight: This is the sharpest executive signal in the survey. Roughly half of both banks and credit unions are not very confident in their ability to deliver personalized, relevant experiences across channels. The issue is not whether personalization is desirable; it is whether institutions have the integrated data, consent, content, decisioning, and measurement systems needed to execute it reliably.

Executive Implication: Personalization requires integrated data, content, analytics, and decisioning.

Why this matters ...

- Consumers increasingly expect relevant recommendations, proactive communications, and seamless experiences tailored to their needs. [17] [18]

- Personalization effectiveness depends on unified data, consent management, content operations, and real-time decisioning, not just marketing technology. [19]

- Institutions that fail to improve personalization capabilities may struggle to deepen relationships, increase engagement, and grow wallet share. [17] [18]

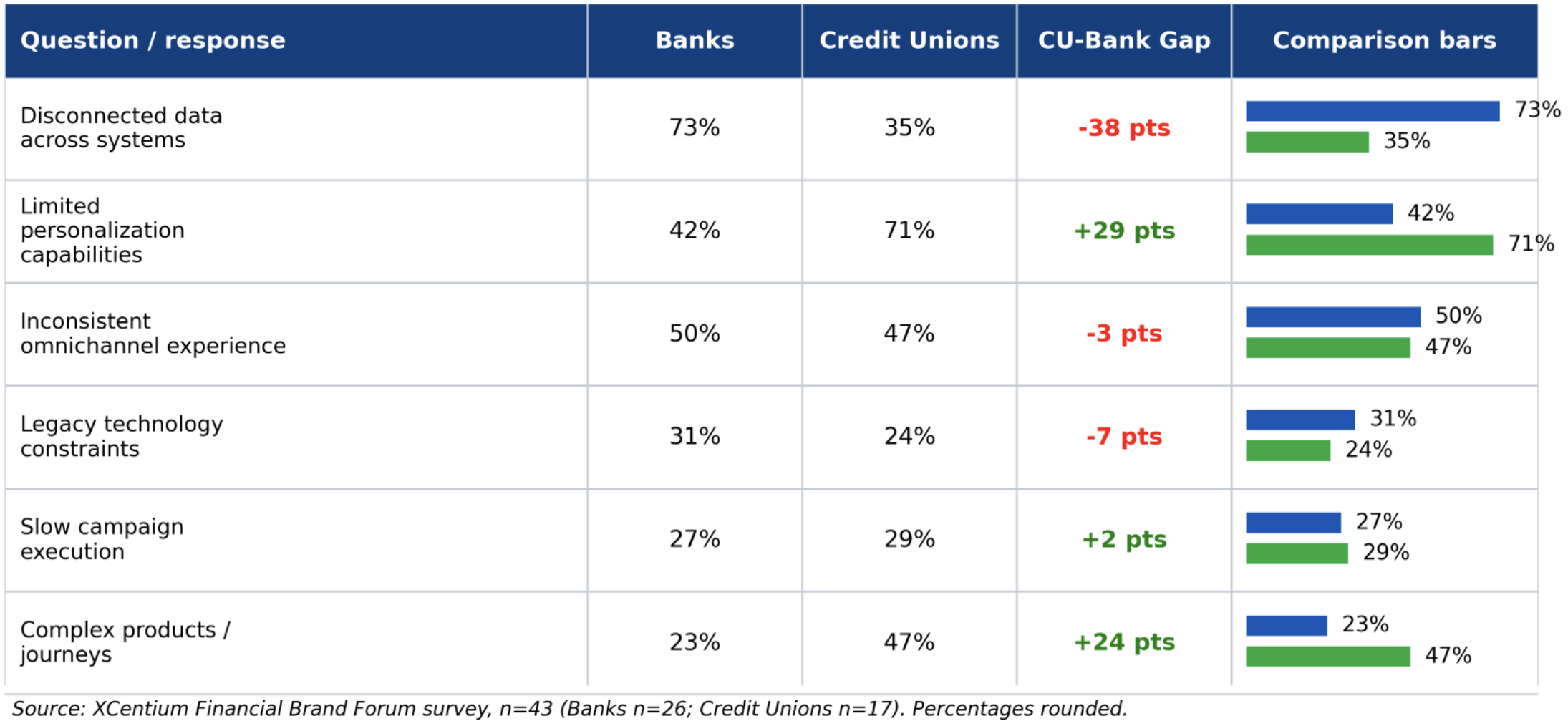

5. Friction and Tech Stack Complexity: Data Fragmentation Is Holding Back Growth

73% of banks cite disconnected data, while 71% of credit unions cite limited personalization capabilities.

Insight: Banks overwhelmingly identify disconnected data as the primary friction point. Credit unions are much more likely to cite limited personalization and difficulty supporting complex journeys. The distinction is important: banks may need to prioritize data unification and activation, while credit unions may need to focus on journey design, segmentation, content relevance, and member-level personalization.

Executive Implication: Banks need data activation. Credit unions need personalization execution.

Why this matters ...

- Data fragmentation remains one of the biggest barriers to delivering consistent, connected customer experiences. [20] [21]

- As customer journeys become more complex, institutions must balance operational efficiency with personalization and engagement goals. [21] [22]

- Reducing friction across data, content, and channel ecosystems can improve marketing agility, customer satisfaction, and organizational productivity. [20] [22]

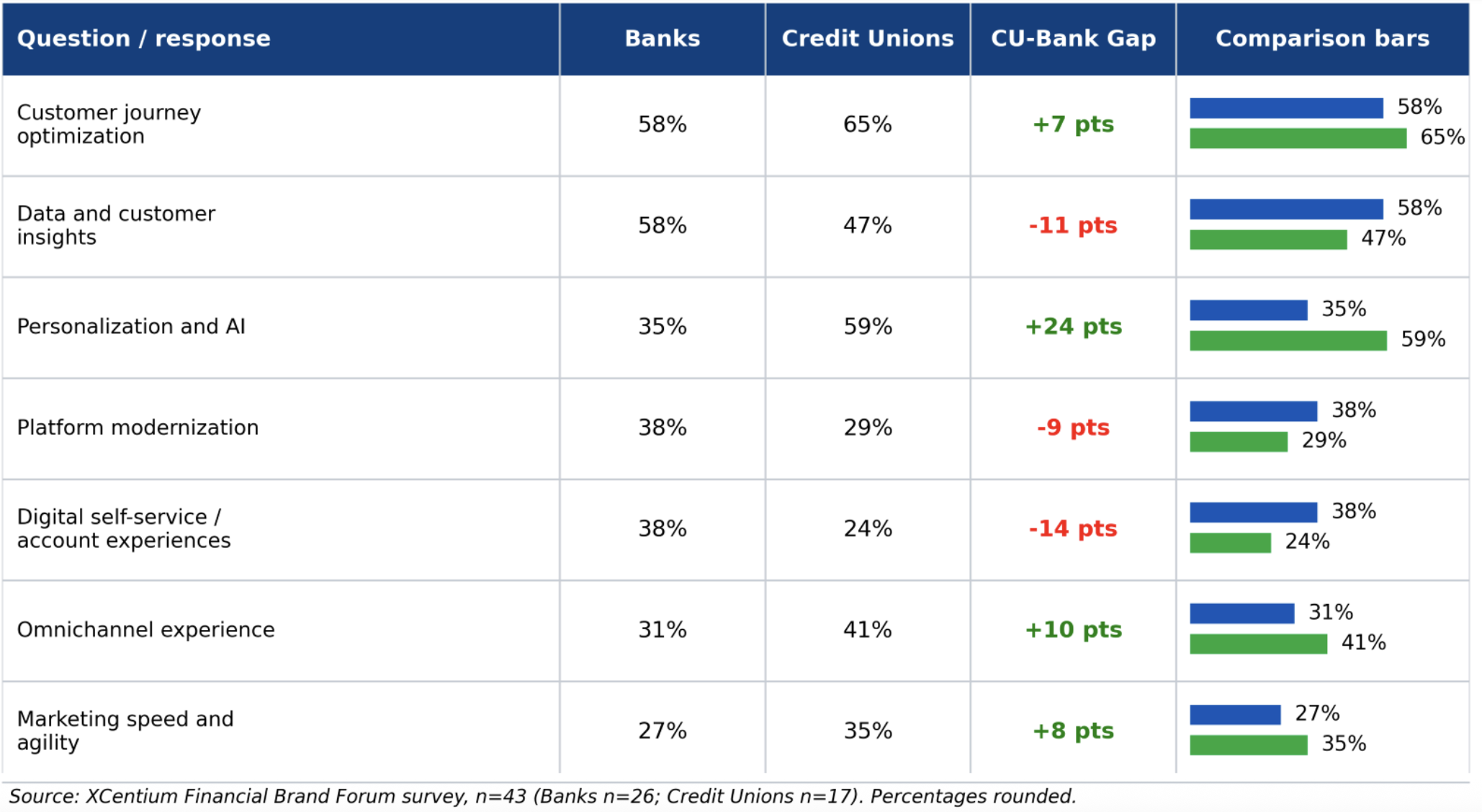

6. Priority Signals: Journey Optimization Is the New Battleground

Customer journey optimization is the top priority across both audiences.

Insight: Both groups place customer journey optimization at the top, making it the clearest shared priority. Banks over-index on data, insights, platform modernization, and digital self-service. Credit unions over-index on personalization, AI, omnichannel experience, and marketing agility. The implication: banks are prioritizing the foundation; credit unions are prioritizing the engagement layer. Both need both.

Executive Implication: The competitive advantage lies in reducing friction across end-to-end journeys.

Why this matters ...

- Customer journey optimization has emerged as the clearest shared priority across banks and credit unions, signaling a shift from channel-focused initiatives to end-to-end experience design. [23] [25]

- Institutions are increasingly recognizing that data, AI, Personalization, and self-service capabilities must work together to support customer goals. [23] [24]

- Organizations that can simplify journeys while improving speed, relevance, and consistency will be better positioned to compete for both growth and loyalty. [24] [25]

Key Similarities Across Banks and Credit Unions

- Customer journey optimization is the unifying priority. Both audiences recognize that the next phase of growth depends on reducing friction across complex, multi-touch journeys.

- Personalization confidence is weak across the board. Very few respondents describe themselves as highly confident, which makes personalization a strategic opportunity and an execution risk.

- AI remains practical, not fully scaled. Most institutions are either exploring, piloting, or using AI in specific areas. The market has moved beyond curiosity, but not yet into broad operating-model transformation.

- Digital experience is functional but not differentiated. The center of gravity is “strong but not a competitive advantage” or “functional but inconsistent,” which means many institutions are vulnerable to competitors with simpler, faster, more personalized journeys.

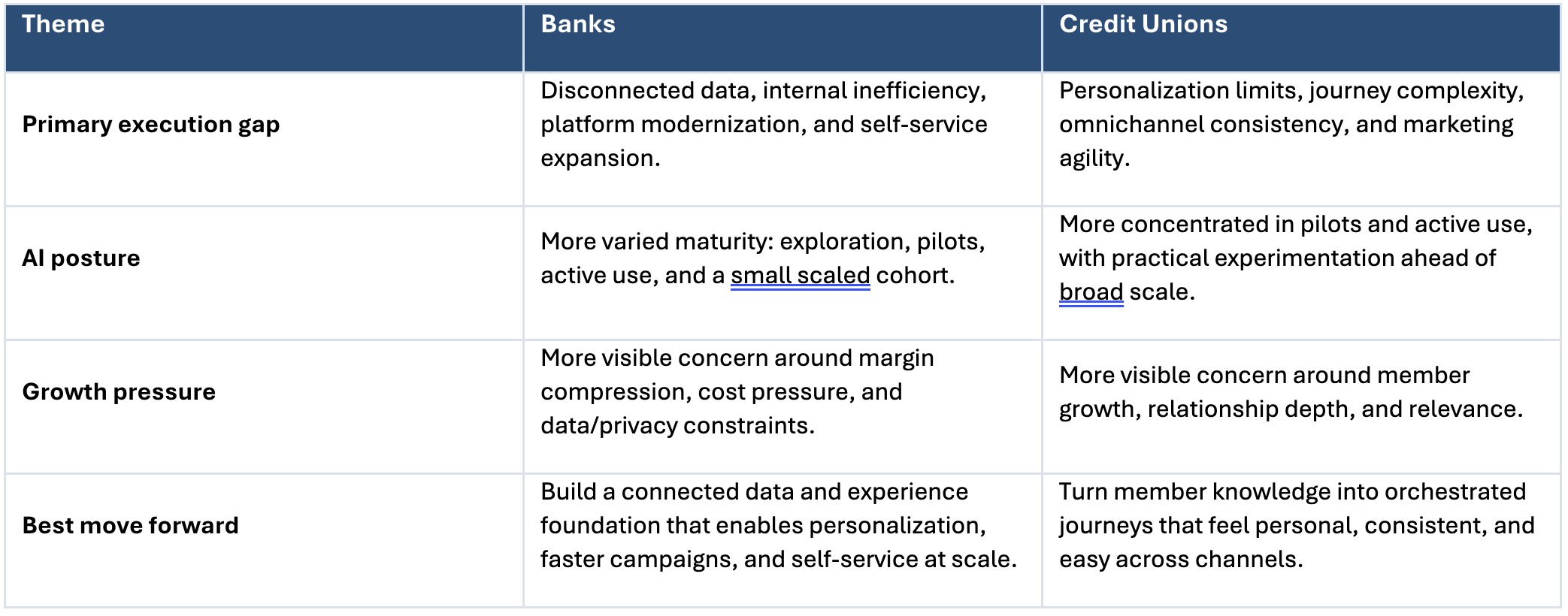

Key Differences: Banks vs. Credit Unions

Execution Gaps to Close

- Data-to-experience gap — Institutions collect meaningful customer and member data, but many cannot activate it consistently across channels. This limits personalization, campaign relevance, and journey measurement.

- AI-to-operating-model gap — AI pilots are moving, but value will remain uneven without governance, use-case prioritization, integrated data, and workflow adoption.

- Content-to-channel gap — Marketing teams need more than content volume. They need modular, governed content that can be personalized, reused, measured, and adapted quickly.

- Journey-to-technology gap — Journey optimization requires coordination across CMS, CRM, analytics, marketing automation, data platforms, identity, forms, application flows, and servicing channels.

What This Means

This year will separate institutions that improve digital touchpoints from institutions that redesign the system behind the touchpoints. Banks and credit unions do not need more disconnected transformation programs. They need an execution model that connects data, content, journeys, AI, governance, and measurement into a repeatable way of working.

- Make customer journey optimization the organizing principle, not just a UX project.

- Prioritize data activation over data collection; the value is in what teams can use in real time.

- Treat personalization as an enterprise capability that requires consent, content, decisioning, analytics, and governance.

- Move AI from isolated pilots to governed, measurable use cases tied to growth, efficiency, service, and risk outcomes.

- Modernize selectively: replace or integrate the parts of the stack that block speed, relevance, and omnichannel consistency.

The most competitive institutions will not be the ones with the longest roadmap. They will be the ones that can turn insight into experience faster, with fewer handoffs and clearer accountability.

Methodology Notes

This report was developed to better understand how banks and credit unions are approaching customer experience, personalization, AI adoption, data integration, and digital transformation priorities. The findings reflect responses collected from financial services professionals who attended the Financial Brand Forum and are intended to provide industry leaders with practical insights into the opportunities and challenges shaping digital strategy today.

The findings are based on 43 Financial Brand Forum attendees who participated in our survey. Survey responses: 26 banks and 17 credit unions. Percentages are rounded to whole numbers. Multi-select questions are shown as the percentage of respondents in each audience segment selecting each option; totals may exceed 100%. Open-ended answers were reviewed directionally but not used as statistically projectable findings.

Public Sources

- FDIC. 2023 FDIC National Survey of Unbanked and Underbanked Households / FDIC press release, Nov. 12, 2024. Mobile banking primary account access: 48.3%. https://www.fdic.gov/news/press-releases/2024/fdic-survey-finds-96-percent-us-households-were-banked-2023

- American Bankers Association / Morning Consult. Consumer Survey Banking Methods, Nov. 22, 2024. Mobile apps used most often by 55% of bank customers; online banking by 22%. https://www.aba.com/about-us/press-room/press-releases/consumer-survey-banking-methods-2024

- Deloitte. 2026 Banking and Capital Markets Outlook, Oct. 30, 2025. Notes AI implementation constraints including fragmented data, compliance demands, legacy systems, and isolated POCs. https://www.deloitte.com/us/en/insights/industry/financial-services/financial-services-industry-outlooks/banking-industry-outlook.html

- U.S. Government Accountability Office. Artificial Intelligence: Use and Oversight in Financial Services, GAO-25-107197, May 19, 2025. https://www.gao.gov/products/gao-25-107197

- Wipfli. State of Credit Unions Report, 2025. 57% of credit union respondents said data analytics/AI was a top strategy in 2025. https://www.wipfli.com/insights/research/-/media/9ba79c72aa2841ca8a6631441a53ecaa.ashx

- Jack Henry / FinXTech. 2025 FinXTech Credit Union Survey. Reported focus areas include chatbots/automated communications (53%), digital retail account opening (49%), and enterprise AI tools (49%). https://www.jackhenry.com/hubfs/resources/reports/2025-FinXTech-Credit-Union-Survey.pdf

- CSI. 2026 Banking Priorities Executive Report. Reported cybersecurity preparedness gap: overall 83%, community banks 85%, credit unions 72%. https://go.csiweb.com/rs/996-ERF-896/images/WP_NPT_MER_BankingPriorities26.pdf

- Federal Deposit Insurance Corporation (FDIC). 2023 National Survey of Unbanked and Underbanked Households. Published November 2024. Reported that 48.3% of banked U.S. households primarily access accounts through mobile banking. https://www.fdic.gov/news/press-releases/2024/fdic-survey-finds-96-percent-us-households-were-banked-2023

- American Bankers Association (ABA) / Morning Consult. Consumer Banking Survey, 2024. Found that 55% of consumers most frequently use mobile banking apps while 22% primarily use online banking. https://www.aba.com/about-us/press-room/press-releases/consumer-survey-banking-methods-2024

- J.D. Power. 2025 U.S. Banking Mobile App Satisfaction Study. Highlights increasing consumer expectations around digital experience quality, personalization, and ease of use. https://www.jdpower.com/business/press-releases/2025-us-banking-mobile-app-satisfaction-study

- Deloitte. 2026 Banking and Capital Markets Outlook. Notes fragmented data environments, legacy technology constraints, and integration challenges as barriers to transformation. https://www.deloitte.com/us/en/insights/industry/financial-services/financial-services-industry-outlooks/banking-industry-outlook.html

- McKinsey & Company. Global Banking Annual Review 2025. Identifies technology modernization and data integration as critical priorities for improving efficiency and growth. https://www.mckinsey.com/industries/financial-services/our-insights/global-banking-annual-review

- Accenture. Banking Technology Vision 2025. Highlights the importance of connected data ecosystems and integrated customer experiences. https://www.accenture.com/us-en/insights/banking

- U.S. Government Accountability Office (GAO). Artificial Intelligence: Use and Oversight in Financial Services. GAO-25-107197. Published May 19, 2025. https://www.gao.gov/products/gao-25-107197

- Wipfli. State of Credit Unions Report 2025. Found 57% of credit union respondents identified data analytics and AI among their top strategic priorities. https://www.wipfli.com/insights/research

- Jack Henry / FinXTech. 2025 Credit Union Technology Survey. Reported planned or current focus on enterprise AI tools, chatbots, and digital account opening capabilities. https://www.jackhenry.com/resources

- Salesforce. State of the Connected Customer, 6th Edition. Reports rising customer expectations for personalized and relevant interactions. https://www.salesforce.com/resources/research-reports/state-of-the-connected-customer

- PwC. Future of Customer Experience in Financial Services. Highlights personalization as a primary driver of customer loyalty and growth. https://www.pwc.com/us/en/services/consulting/library/customer-experience.html

- Deloitte Digital. Personalization at Scale in Financial Services. Discusses the data, content, governance, and decisioning requirements needed to deliver effective personalization. https://www.deloitte.com

- Gartner. Top Strategic Technology Trends for Banking, 2025. Highlights platform complexity, technical debt, and fragmented customer data as major challenges. https://www.gartner.com/en/industries/banking-and-investment-services

- Forrester. Predictions 2026: Financial Services. Discusses the operational impact of fragmented technology ecosystems and disconnected customer journeys. https://www.forrester.com/predictions

- Cornerstone Advisors. What’s Going On In Banking 2026. Identifies operational efficiency, technology modernization, and customer experience improvement as leading strategic priorities. https://www.crnrstone.com

- The Financial Brand. Digital Banking Trends and Priorities Report 2026. Highlights customer journey optimization, personalization, and omnichannel experience as top investment areas. https://thefinancialbrand.com

- CSI. 2026 Banking Priorities Executive Report. Identifies customer experience, operational efficiency, cybersecurity, and digital modernization as key focus areas. https://go.csiweb.com/rs/996-ERF-96/images/WP_NPT_MER_BankingPriorities26.pdf

- Accenture. Banking Top 10 Trends for 2026. Discusses journey-centric operating models, AI-enabled engagement, and customer-centric transformation priorities. https://www.accenture.com/us-en/insights/banking

Author

Sue Nunez

Sales Director

Sue boasts over two decades of experience in both the MarTech and SaaS space. Known for fostering collaboration, strategic thinking, and long-lasting client relationships, she has a wide range of industry experience including financial, retail, healthcare, manufacturing and more.